The U.S. Bureau of Economic Analysis's (BEA) first estimate of third quarter annualized real gross domestic product (GDP) growth released on October 28 was 2.9 percent. A number of nowcasts were quite close to this number, including the median forecast of 3.0 percent from the CNBC Rapid Update survey![]() of roughly 10 economists. The Atlanta Fed's GDPNow model forecast of 2.1 percent? Not so close.

of roughly 10 economists. The Atlanta Fed's GDPNow model forecast of 2.1 percent? Not so close.

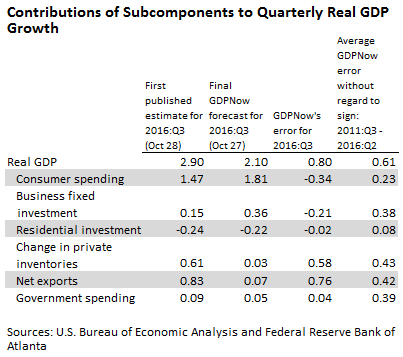

What accounted for GDPNow's miss? The table below shows the GDPNow forecasts and BEA estimates of the percentage point contributions to third quarter growth of six subcomponents that together make up real GDP. The largest forecast error, both in absolute terms and relative to the historical accuracy of the projections, was for the contribution of real net exports to growth. The published contribution of 0.83 percentage points was much higher than the model's estimate of 0.07 percentage points.

Why did GDPNow miss so badly on net exports? For both goods and services real net exports, the GDPNow forecast is a weighted average of two forecasts. The "bean counting" forecast uses the monthly source data on the nominal values and price deflators of exports and imports. The econometric model forecast uses published values of 13 subcomponents of real GDP for the last five quarters to predict real net exports for both goods and services. The statistically determined weights on the bean counting forecast increase as we get closer to the first GDP release and accumulate more monthly source data. (More details are provided here.)

For real net exports of services, 89 percent of the weight was given to the bean counting forecast. This weighting worked out well last quarter as the forecasts of the contribution of real services net exports to third quarter growth from both the bean counting and combined models were within 0.01 percentage points of the published value of −0.14 percentage points. But for real net exports of goods, the bean counting forecast received only 59 percent of the weight in the final GDPNow forecast. It projected that real net exports of goods would add 0.76 percentage points to growth—reasonably close to the BEA estimate. In contrast, the econometric model projected a subtraction of 0.58 percentage points from growth.

Since GDPNow had monthly price and nominal spending data through September on goods imports and exports, why didn't it place more weight on the source data? One of the important reasons is that it's difficult to match the quarterly inflation rate of the BEA's import price deflator for goods. The BEA constructs its price deflator ![]()

![]() with detailed price indices from the Bureau of Labor Statistics (BLS) producer price index and import/export price index programs as well as a few other sources. GDPNow uses the BLS's import price data at higher levels of aggregation than the BEA uses and also differs in the manner that it handles seasonality. The chart below plots the difference between the BEA's quarterly goods import price inflation rate and the GDPNow proxy. These inflation measures have differed by 5 percentage points or more on a number of occasions. Since goods imports are 12 percent of GDP, a miss of this magnitude on the price deflator would lead to a miss on the real net exports of goods contribution to growth of 0.5 percentage points or more, even if the other ingredients in the calculation were all correct.

with detailed price indices from the Bureau of Labor Statistics (BLS) producer price index and import/export price index programs as well as a few other sources. GDPNow uses the BLS's import price data at higher levels of aggregation than the BEA uses and also differs in the manner that it handles seasonality. The chart below plots the difference between the BEA's quarterly goods import price inflation rate and the GDPNow proxy. These inflation measures have differed by 5 percentage points or more on a number of occasions. Since goods imports are 12 percent of GDP, a miss of this magnitude on the price deflator would lead to a miss on the real net exports of goods contribution to growth of 0.5 percentage points or more, even if the other ingredients in the calculation were all correct.

Are there any lessons here for improving GDPNow? Ideally, GDPNow would be able to closely map the monthly source data to real goods net exports so that most of the weight would go to the bean counting forecast once all of the data are in—much as it does with nonresidential structures and residential investment. The BEA's estimates of real petroleum imports are based on similar data in the monthly international trade data publication. Because petroleum imports account for so much of the volatility of inflation for goods imports, it may be better to use the monthly real petroleum imports data directly and only worry about replicating the price index for nonpetroleum goods.

That said, a previous macroblog post illustrated that the method GDPNow currently uses has a reasonable forecasting track record for net exports when compared with several consensus estimates from professional forecasters. Net exports may remain difficult to nowcast even with refinements to GDPNow's methodology.

GDPNow has established a commendable track record. But sometimes when it misses the mark, an analysis of the error can provide insight into how GDPNow works and the limitations of the model.

By Pat Higgins, an associate policy adviser and economist in the Atlanta Fed's research department

By Pat Higgins, an associate policy adviser and economist in the Atlanta Fed's research department