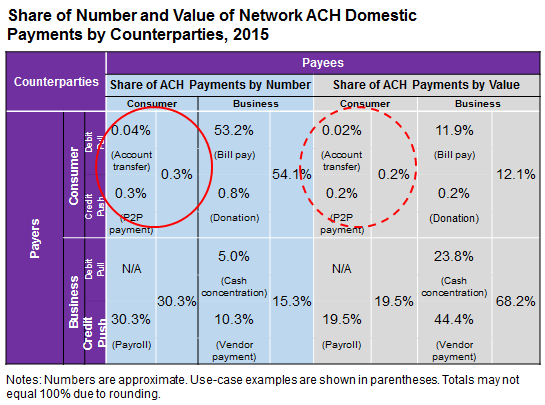

In a post last August, I analyzed some of the data from the inaugural release of the entire aggregated data set of estimated noncash payments from the latest Federal Reserve payments study. In this go-round, I will discuss the household payment figures in the report that accompanied the data set. These figures reflect core noncash payment types—including ACH transfers, check, nonprepaid and prepaid debit cards, and credit cards— that consumers in the United States use today.

The two pie charts show the distribution of household noncash payments for 2000, when the payments study began, and for 2015. Over this period, the number of consumer payments increased to 117.5 billion in 2015 from 50.7 billion in 2000. The area of each pie chart reflects the proportional difference in the average monthly household noncash payments for the two periods. In 2000, households made on average 40.3 noncash payments per month, compared to 78.6 monthly payments in 2015, a 95 percent increase.

{kind=link}

Besides the near doubling of monthly payments per household, the other striking difference is the distribution of payments by type over time. Most dramatically, checks written decreased 6.4 percent per year over this time while debit cards, with an annual increase of 13.7 percent, were on a tear.

As the report notes, and according to my own speculations, increases in the number of monthly household noncash payments could be attributed to the following factors:

- Some payments that historically would have been made with cash are now made with mostly noncash forms of payment. Debit cards snagged the greatest share, given their high growth rate and relatively low average ticket amount, which aligns with payments typically made with cash.

- Storefront merchants and consumers have expanded their acceptance of card payments as a substitute for cash and check.

- The growth of remote payments such as ecommerce have reduced check and cash usage.

- Many people have migrated from using cash and check to using payment cards so they can gain points and other benefits from card rewards programs.

- Online purchases of digital content such as games and music have brought about increases in micropayments.

We might surmise that increases in the number of payments in 2015 are also due to increases in household expenditures since 2000, though this is hard to quantify by number of payments. World Bank data show aggregated U.S. household consumption expenditures of $12.284 trillion and $6.792 trillion (in current dollars) in 2015 and 2000, respectively. Unlike the payments study data, these figures include both cash and noncash payments, and some of the expenditures are derived from imputed income related to high-ticket items such as purchases of homes and automobiles. With these caveats in mind, dividing these figures by the number of households during each of these years shows that the per-household expenditures in current dollars is about 52 percent higher in 2015 than it was in 2000. Not all of this gain came about from more payments—some payments may be higher ticket amounts than in previous periods due to luxury purchases.

What are your views on other factors contributing to the near doubling of monthly household noncash payments since 2000?

By Steven Cordray, payments risk expert in the Retail Payments Risk Forum at the Atlanta Fed

By Steven Cordray, payments risk expert in the Retail Payments Risk Forum at the Atlanta Fed